Table of Contents Show

Financial literacy is an essential skill that should be developed throughout our lives. By teaching financial concepts from a young age and revisiting them as we grow, we can build a strong financial foundation.

One important aspect of financial education that is often overlooked is estate planning, which is crucial for long-term financial well-being. In this article, we will discuss how financial education should adapt at various stages of life.

Childhood (Ages 5–12): Laying the Foundation for Financial Understanding

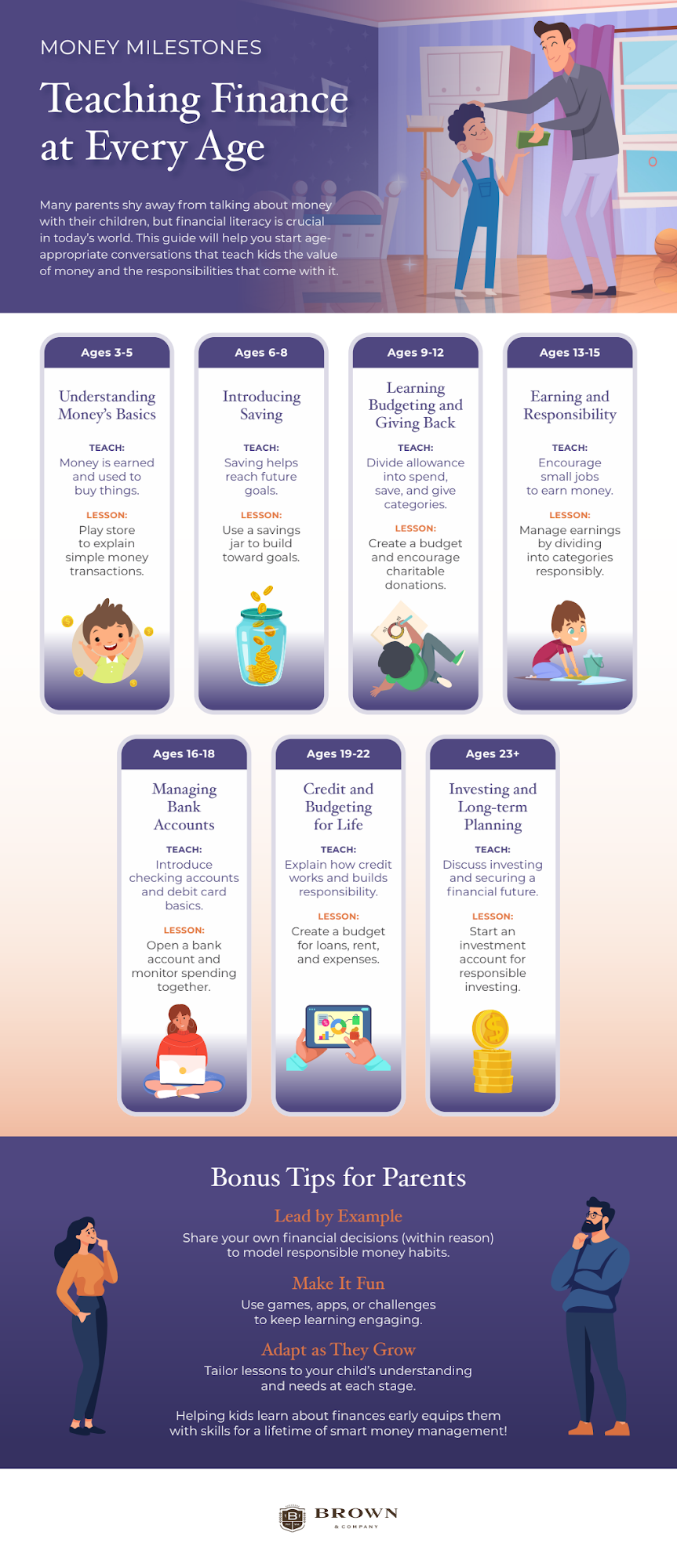

The earlier a child is introduced to financial concepts, the better equipped they will be to manage money as they grow. During this stage, parents and teachers should focus on simple but essential concepts, including:

- Understanding Money: Helping kids learn about different currency denominations and how they can be used for purchases.

- Saving and Spending: Use piggy banks or savings jars to show how money accumulates and the importance of saving.

- Earning Money: Encourage small chores or tasks in exchange for an allowance to build a sense of earning.

- Needs vs. Wants: Teaching the difference between essential items and things we desire.

Even at this young age, parents can introduce the basics of estate planning by discussing inheritance, like how family treasures or possessions are passed down from one generation to the next.

Teenage Years (Ages 13–19): Budgeting, Credit, and Smart Spending

As teenagers gain more independence, it’s important to teach them about managing money responsibly. Key lessons during this period should include:

- Budgeting: Teaching teens to manage income from allowances or part-time jobs by budgeting for needs and wants.

- Bank Accounts: Encouraging the opening of a savings or checking account to introduce concepts like deposits, withdrawals, and bank fees.

- Credit and Debt: Explaining how credit works, the impact of credit scores, and the dangers of accumulating debt.

- Investment Basics: Introducing the concept of investing in stocks, bonds, and mutual funds to help them understand long-term wealth-building.

Teenagers can also begin to understand the importance of estate planning by learning why it’s important to have a will and what the role of beneficiaries is.

Young Adulthood (Ages 20–35): Building Wealth and Financial Independence

In young adulthood, financial choices start to shape long-term outcomes. Key financial lessons should include:

- Emergency Fund: Teaching the importance of setting aside money to cover unexpected expenses, aiming for three to six months’ worth of living expenses.

- Retirement Savings: Explaining the basics of retirement accounts such as 401(k)s and IRAs, and the importance of starting early.

- Debt Management: Helping young adults develop strategies to manage student loans, credit card debt, and other obligations.

- Homeownership: Introducing concepts related to mortgages, down payments, and how to save for a first home.

- Insurance: Emphasizing the need for health, life, and disability insurance as a safeguard for financial security.

This stage is also an opportune time for young adults to begin estate planning by designating beneficiaries for accounts and considering a basic will to ensure their wishes are carried out.

Midlife (Ages 36–55): Securing and Expanding Wealth

At this stage, individuals should focus on protecting and growing their wealth while also preparing for future goals like retirement. Important financial concepts include:

- Maximizing Retirement Contributions: Teaching the importance of fully contributing to retirement plans such as 401(k)s and IRAs.

- Diversifying Investments: Encouraging investments in various assets to build wealth and minimize risk.

- College Savings Plans: Discussing savings options like 529 plans for children’s higher education.

- Comprehensive Estate Planning: Guiding individuals to draft a detailed will, set up trusts, and designate a power of attorney.

This is also the time to start serious estate planning, ensuring that assets will be distributed according to one’s wishes and that loved ones are taken care of.

Retirement and Beyond (Ages 56+): Preserving Wealth and Legacy Planning

As retirement draws near, financial education shifts to focus on maintaining a steady income and managing wealth efficiently. Key financial principles include:

- Withdrawal Strategies: Teaching how to manage retirement savings so that funds last throughout retirement.

- Tax-Efficient Investment Management: Focusing on how to reduce taxes while preserving wealth.

- Long-Term Care Planning: Discussing how to prepare for potential healthcare needs in older age.

- Estate Planning Updates: Ensuring wills and trusts are up to date and that healthcare proxies and power of attorney are designated.

At this stage, estate planning takes center stage as individuals solidify their legacy, ensuring smooth transitions for heirs and loved ones.

Conclusion

Financial education is important at every stage of life. By teaching the basics of money management, saving, investing, and estate planning, individuals can be better prepared for the future. Introducing estate planning alongside everyday financial lessons helps individuals achieve financial independence and secure their financial legacy for future generations. Teaching finance throughout life leads to long-term financial security and peace of mind.

Infographic

Infographic provided by Brown & Company, a top place for estate planning in Denver CO

Infographic provided by Brown & Company, a top place for estate planning in Denver CO